Key takeaway

- A no chain purchase means that there are no linked sales above you, meaning you are only dealing with yourself, your seller, your lending party, and your legal team.

- Even without the benefit of a chain, for most mortgage buyers, buyers should expect about 30 to 45 days from accepted offer to closing, and for some cash buyers, they may be able to close in two weeks.

- A chain free sale has the same basic steps as any other purchase such as the offer, legal checks, inspections, appraisal, mortgage approval and finally the closing.

- You can expedite a no chain buy by preparing ahead of time; seeking strong pre approval; selecting your attorney ahead of time; and responding promptly to any document requests.

- Delays can still occur in a chain free deal if inspections show major issues, the appraisal comes in low, title issues arise, third party paperwork is slow, or your finances change.

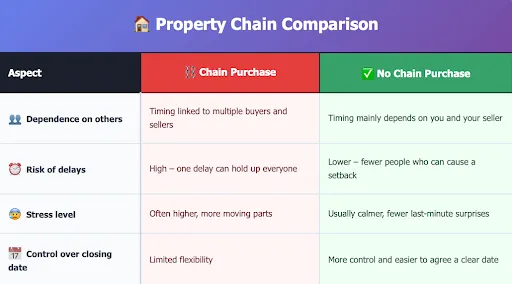

- Compared to a chain purchase, a no chain deal tends to be calmer and more predictable, so you have more control in timing even though it cannot necessarily have instant keys.

Buying a home is often described as one of the most stressful life events, but purchasing a property with no chain can significantly reduce that pressure. In simple terms, a no chain house purchase means your transaction is not dependent on another buyer or seller completing their own move. There is no domino effect. No waiting for someone else’s mortgage approval. No delays caused by another family trying to close on a different property.

For buyers in competitive markets like Long Island, understanding the typical timeline for a no chain house purchase can help you plan realistically, avoid surprises, and position yourself for a smoother closing.

What Does “No Chain” Really Mean?

A property chain forms when multiple transactions are linked together. For example, the seller of your future home may need to sell that property in order to buy another one. That seller’s new purchase may depend on yet another transaction. If one deal falls apart, every linked deal can collapse or stall.

A no chain purchase removes this dependency. The seller is either not buying another property or has already secured their next home. This is common with vacant properties, estate sales, investor-owned homes, new construction, or sellers who have already relocated. Buyers can also be chain free if they are first-time purchasers or cash buyers.

The key advantage is independence. Your timeline is not tied to anyone else’s transaction.

How Long Does a No Chain House Purchase Take?

In most cases, a no chain house purchase takes approximately 30 to 45 days from offer acceptance to closing when financing is involved. This is considered a standard mortgage timeline in many U.S. markets, including Long Island.

If the buyer is paying in cash and title work progresses smoothly, the process can close in as little as two to three weeks. However, speed depends on preparation, responsiveness, and the absence of legal or inspection complications.

It is important to understand that while removing a chain eliminates one major source of delay, it does not eliminate the legal and financial requirements involved in transferring property ownership.

The Real Process Behind the Timeline

Once an offer is accepted, the transaction enters its formal phase. The buyer’s attorney or title company begins reviewing contracts and initiating the title search. If a mortgage is required, the lender moves the application into underwriting. Inspections are scheduled to evaluate the condition of the property, and the lender orders an appraisal to confirm its market value.

During this period, documentation becomes critical. Lenders verify income, employment, credit history, and assets. Any missing paperwork can delay underwriting. At the same time, the title search ensures there are no liens, ownership disputes, or legal encumbrances attached to the property.

After inspections and appraisal are completed, negotiations may occur if repairs are required or if the valuation differs from the contract price. Once all contingencies are cleared and loan approval is finalized, the transaction moves toward closing. Final documents are prepared, funds are transferred, and ownership is officially recorded.

Even in a no chain deal, these steps require coordination and compliance with legal standards.

Why No Chain Does Not Always Mean Instant Closing

Many buyers assume that no chain equals immediate key handover. In reality, financing remains the largest factor affecting speed. Mortgage underwriting involves risk assessment and regulatory compliance. Appraisal scheduling can depend on local availability. Title searches sometimes uncover unexpected issues, particularly in older Long Island homes where permits, boundary adjustments, or prior liens may exist.

Inspection findings can also influence the timeline. Structural concerns, roof damage, plumbing problems, or electrical updates may require additional evaluation or negotiation. While these issues are not related to a property chain, they still impact how quickly a transaction can close.

Local administrative processes can also add time. In certain Long Island municipalities, open permits or certificate of occupancy discrepancies must be resolved before closing. These are common hurdles that buyers should anticipate, regardless of chain status.

Step by step timeline of buying a no chain property

Thinking in steps makes the process feel less mysterious. Below is a step by step route that many chain free buyers follow, with rough timing.

Step 1: Offer and acceptance

You look at the property and agree on a price and both parties sign the purchase agreement. With no chain, this stage is often quicker as the seller is not waiting on another move.

Step 2: Hire your attorney or closing agent

As soon as your offer is accepted timely, you appoint your attorney or title company. They open the file, request the contract, and get started on the title search so that the case does not sit idle.

Step 3: Apply for your mortgage if needed

If you require a loan, you complete your full mortgage application and upload all of the documents that are requested. Having pre-approval in place can shorten this step and reduce stress.

Step 4: Book inspections and appraisals

You arrange for your home inspection to take place as early as possible in your contract and the lender arranges for an appraisal to be ordered to ensure the value. Appraisal may still be chosen by cash buyers, but can then be more flexible in timing.

Step 5: Review title and legal checks

Your attorney or title company confirms the seller can legally transfer the property and checks for liens or record mismatches. Minor issues are usually resolved with the seller before closing.

Step 6: Remove contingencies

When you have inspection, appraisal, and loans in place you sign to get rid of contingencies. This converts the deal from conditional to firm, and allows everyone to concentrate on the closing date.

Step 7: Final figures and closing day

You review your closing statement, send your funds, and sign the final documents. You’ve finally got the keys in your hand after the deed has been recorded and you’ve officially taken possession of the home.

Market Conditions in Long Island

The Long Island housing market can be competitive and fast-moving, but that does not always translate to faster closings. In busy periods, inspectors, appraisers, and attorneys may have full schedules. Even when both buyer and seller are motivated, professional availability can shape the timeline.

Additionally, older properties in Nassau and Suffolk Counties often come with historical modifications. Deck additions, finished basements, and structural alterations sometimes require documentation updates before transfer. A knowledgeable local real estate professional can identify these issues early, preventing last-minute delays.

How Buyers Can Shorten the Timeline

Preparation is the most powerful tool in a no chain purchase. Buyers who secure full mortgage pre-approval before making an offer often move through underwriting more efficiently. Organizing financial documents in advance prevents repeated lender requests. Scheduling inspections immediately after contract signing reduces bottlenecks.

Clear communication between attorney, lender, agent, and title company also plays a major role. Delays often occur not because of complexity, but because of slow responses. Buyers who remain financially stable during escrow, avoiding new debt or employment changes, protect their approval status and prevent re-underwriting.

Cash buyers, while faster in many cases, still benefit from professional title review and due diligence to avoid future legal complications.

No Chain vs. Chain Transactions: The Practical Difference

The absence of a chain reduces uncertainty. In chain transactions, multiple families must align moving schedules, financing approvals, and contract contingencies. If one buyer’s loan falls through, every connected deal is affected.

In a no chain purchase, the focus remains solely on your transaction. While inspections, financing, and legal checks still apply, there is no external dependency that can collapse the agreement without warning. This typically results in greater predictability and lower emotional stress.

Final Thoughts

A no chain house purchase offers a significant advantage in terms of control and efficiency. In Long Island, most financed transactions close within 30 to 45 days, while cash deals may close in two to three weeks when properly prepared. Although the absence of a chain reduces risk, the transaction still requires careful coordination, legal review, financial approval, and thorough inspection.

Understanding the true timeline helps buyers set realistic expectations and avoid unnecessary anxiety. With preparation, experienced guidance, and proactive communication, a no chain purchase can be one of the smoothest paths to homeownership.

If you are considering buying or selling a chain-free property in Long Island, working with knowledgeable local professionals ensures that your timeline remains steady and your transaction progresses with clarity from offer to closing.

Frequently Asked Questions

How fast can I buy a no chain house with cash?

If you are purchasing with cash, and the property has a clear title then you may be able to close within two weeks. The primary limitations will be how quickly you can get the inspections, title work done, and closing documents signed.

Is a no chain house always cheaper?

Not always. Some sellers may even charge a chain free home just higher as it is more appealing to buyers that value speed as well as certainty. You still have to check recent sales, the condition of the properties, and the local market to determine whether the price is reasonable or not.

How do I make my offer more attractive on a no chain property?

You can enhance your offer by showing good proof of funds or good pre approval for a mortgage loan, reasonable timelines and a flexibility in moving dates. Clear communication and a responsive attorney also help the seller feel that your deal is going to actually make it to the closing table.